Economic Overview

Global share markets continued their revival in the first quarter of 2013, with the returns from companies in developed economies outpacing bonds and commodities. Even so, the positivity from continually rising share markets masked more mixed underlying conditions.

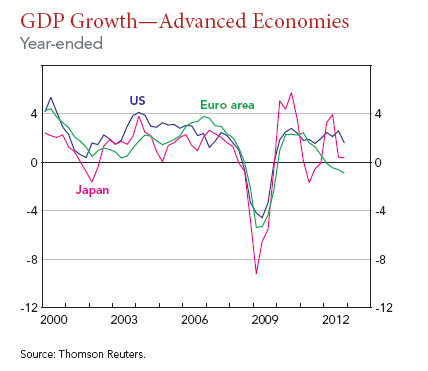

Again, risk assets were embraced as monetary stimulus continued and the US showed its economic recovery was gathering pace. However, the major questioned remained – when would the US Federal Reserve begin to signal an end its ongoing monthly stimulus program?

In Japan, the newly elected government looked to end two decades of deflation by weakening the yen. In early April it announced an unprecedented $1.4 trillion stimulus to lift inflation.

In China, manufacturing growth showing significant signs of slowing and export growth decelerated due to weaker demand in developed economises. This in turn hit commodity prices.

In Europe, worries over the single currency zone emerged again as Cyprus negotiated a deal with lenders to stave off financial collapse. The IMF, ECB and EU gave it an additional two years to implement measures linked to a bailout.

Back in Australia, the Reserve Bank acknowledged there were signs of a peak in resource investment, raising questions of what would take over as the main growth driver. The RBA suggested rate cuts were starting to have an effect as some evidence of a rebound in consumer spending emerged.

Even so, with rates at record lows consumers still showed no inclination to embrace their high borrow and spend ways prior to the financial crisis. This was reflected by weak credit growth and household savings maintaining their strength.

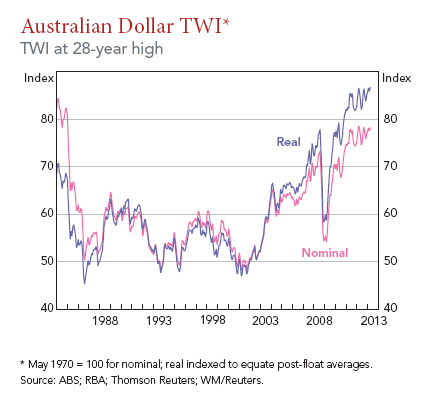

The Australian dollar continued to defy falling commodity prices and the erosion of an interest rates advantage by staying well clear of parity with the US dollar.

Market Overview

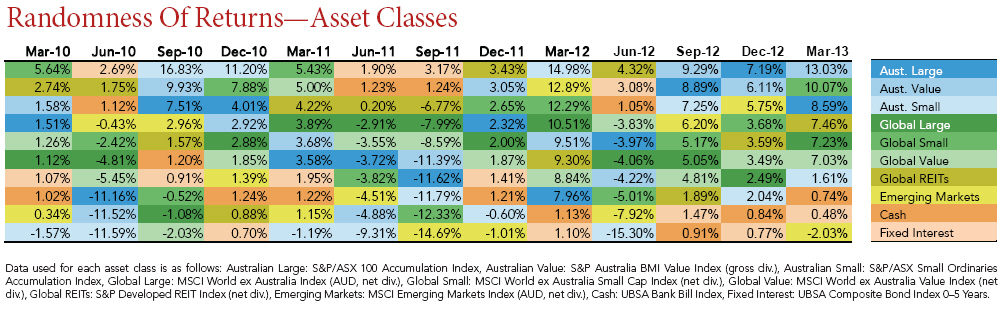

A significant feature of the March quarter was the lack of any global market trend, which again highlighted the benefits of diversification.

The Australian market outperformed most other developed markets, while developed markets outpaced emerging markets.

In a reversal of 2012, value shares outperformed their growth counterparts in Australia, but small caps continued to lag large caps. Small caps suffered as smaller mining shares came under pressure from weaker commodity prices and a slowing China.

All local sectors apart from materials recorded gains; consumer discretionary shares were the standout with better than expected earnings reported from retailers.

While global real estate trusts performed well over the quarter, the Australian sector lagged behind.

Outside Australia other developed markets also performed well, led by Japan and its monetary stimulus. In developed markets, growth shares outperformed value and small shares outperformed large, reversing the results in Australia.

Again, there are few trends to be found over the past three years of quarterly returns. Despite emerging markets providing healthy growth in three of the past four quarters, it slumped to a negative return in the first quarter of 2013. Australian value provided the best returns over the quarter, but go back to June 2012 and it was bringing up the rear by a margin.

Safe Haven Takes a Hit

Gold declined almost 5% over the quarter; it followed this with a significant plunge as we moved into the first half of April. While gold is frequently cited in the media as a safe haven providing stability and a hedge against inflation, the reality is a little different.

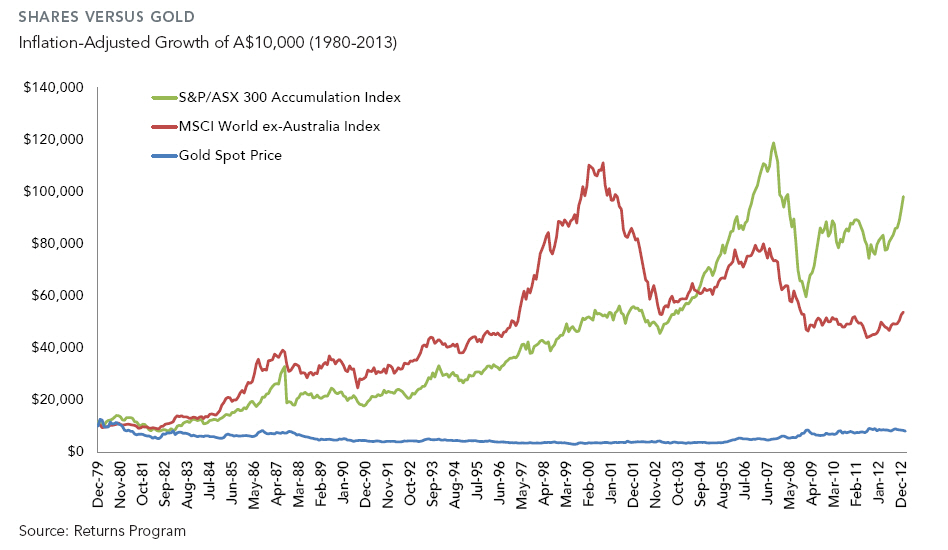

The chart shows the inflation-adjusted returns of Australian shares, global shares and gold from 1980 until February 2013.

If you’d invested $10,000 in the Australian share market in 1980 it would have grown to around $100,000 today. Global markets, as measured by the MSCI World ex-Australia Index would have grown to $54,000.

Gold’s return after adjusting for inflation over three decades? Zero, in fact, you’d be slightly in the red.

All that volatility and no protection against inflation, yet the media continue to refer to gold as a ‘safe haven’. Even worse, some of our more respected financial publications continue to publish maniac headlines like this:

“Safe haven gold is tipped to run up to $3000.” Australian Financial Review, Sept, 27, 2012

We won’t hold our breath.

Insider Signs Off

Finally, Morgan Stanley Global Strategist, Gerard Minack has left the investment bank to start his own business. His parting words again illustrate the futility of active management and paying higher fees in the attempt to outperform the market.

Minack bemoans how short sighted financial markets have become and offers the following on what he calls the financial industry’s “dirty little secret”.

“The average professional underperforms. Investors would be better off buying the index as more often than not, that would beat the pros.”

“What other profession is there where amateurs can beat the pros? If we played tennis against Federer we wouldn’t win a point.”

“If we played a round of golf with Tiger we’d lose. Voters get the politicians they deserve and we three get the fund managers we do because people give them money.”

Minack is backed by S&P Indices Versus Active Funds Scorecard (SPIVA), which once again showed the majority of active funds underperformed their respective benchmarks.

SPIVA’s mid 2012 report showed more than 70% of active Australian retail funds underperformed their benchmarks over a one period and 80% underperformed over a three year period.

More than 88% of active international retail funds underperformed over one year and 80% over three years.

100% of active bond funds underperformed over a one year period and over 85% of listed property (A-REIT) underperformed over one and three years.

It’s hardly a dirty little secret anymore.

With thanks to DFA Australia.

This material is provided for information only. No account has been taken of the objectives, financial situation or needs of any particular person or entity. Accordingly, to the extent that this material may constitute general financial product advice, investors should, before acting on the advice, consider the appropriateness of the advice, having regard to the investor’s objectives, financial situation and needs. This is not an offer or recommendation to buy or sell securities or other financial products, nor a solicitation for deposits or other business, whether directly or indirectly. Wondering who to trust with your financial affairs? We ‘re one of six fiduciary financial planners in Australia.