Economic Overview

Global share markets began strongly in the second quarter of 2013 and the US market hit record highs in May. However the ongoing momentum came to an abrupt halt as the mood shifted and the market moved downwards in late May.

The correction was triggered by suggestions from the US Federal Reserve that it would begin to taper its quantitative easing (QE) program. Currently the US Fed buys $85 billion in bonds each month to keep interest rates low and stimulate economic activity.

While US economic data improved, the markets chose to focus on the stimulus withdrawal. This pulled share markets off their highs, pushed up bond yields and strengthened the US dollar. Compounding the risk retreat were signs China was aiming for a more sustainable growth rate by curbing excessive bank lending. The important area to focus on though is the improvement of the US economy which has prompted the hint of stimulus withdrawal.

Japan defied the weaker Asian trend by leading the markets in the region, providing more evidence of a pickup in the world’s third largest economy.

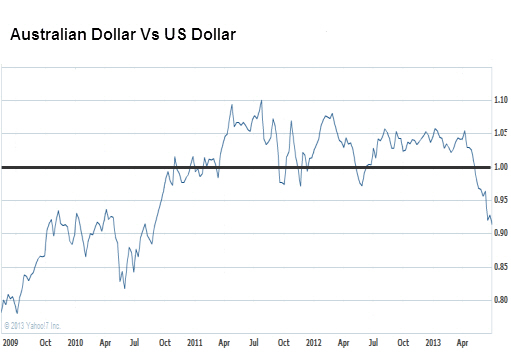

Back in Australia, the economy slowed to a below-trend pace as it began the transition from the resources boom to other sources of growth. The Reserve Bank cut cash rates to record lows in May, noting the Australian dollar had remained stubbornly high despite falling commodity prices and a decline in the terms of trade.

The May interest rate cut and the suggestion of US Federal Reserve tapering combined to send the Australian dollar lower. It moved below parity and hovered near three-year lows, just above the 90 US cent mark. The RBA will be hoping for further declines to help rebalance growth away from mining.

Market Overview

The US Fed’s signalling that it may taper its QE program impacted share, fixed interest, commodity and currency markets. Much of this reflected an unwinding of carry trades, where investors borrow in low-yield interest rate currencies to find higher yield elsewhere.

As US bond yields climbed, the cost of funding high yield trades increased. Consequently, investors sold positions in the Australian dollar, NZ Dollar and Brazilian Real to cover their short US dollar positions. This helped to push the Australian dollar downward and increase returns for international markets in the local currency.

Commodities were substantially weaker, as the US dollar strengthened and China’s appetite was downgraded. Gold’s 23% decline led the way, subsequently punishing listed gold miners around the world, while nickel fell 18% and copper 10%.

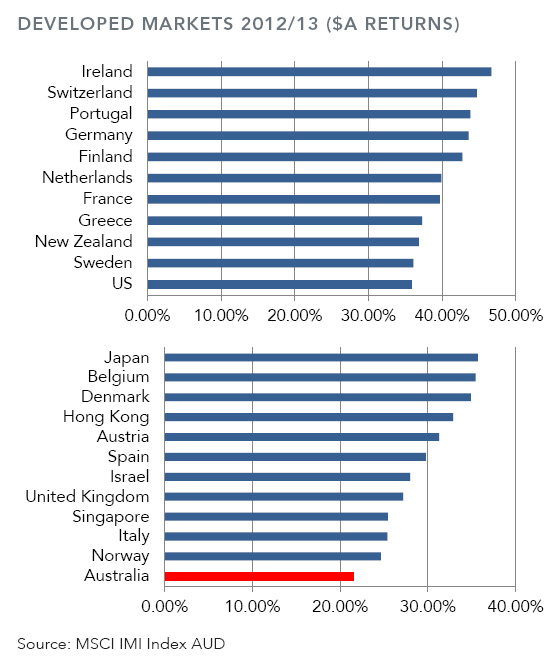

This commodity driven weakness was the biggest drag on the Australian market, while gains came in telecommunications, healthcare and REITs.

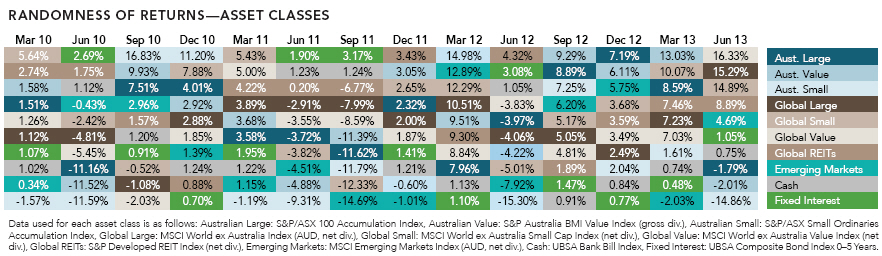

Again, there are few trends to be found over the past three years of quarterly returns. While Australian large and value offered strong returns in the previous three quarters, they finally slipped to negative territory.

The dominant performance of the quarter came from the Global area, with value, large and small all providing double digit returns. After a previous quarter in the red, emerging markets had a solid quarter, while Australian small caps lagged all other classes significantly.

The New Normal

Early in July 2012, The Australian Financial Review offered a grim prognosis for future growth, with the headline, “Low Returns Shape as the New Normal”. Double-digit annual returns were over for shares, as columnist, Tony Boyd rattled off concerns over Greece, Europe and the US & China.

While over at The Australian on the same day, Robin Bromby confidently assured readers that any market recovery “won’t last” and financial Armageddon could be on the way. Developed market returns a year on from these predictions speak for themselves.

Boyd’s article was backed by RBA governor, Glenn Stevens who’d reminded investors that the returns they’d previously achieved leading up to 2008 wouldn’t be repeated for years and maybe not at all.

Be it journalists huffing and puffing for a headline or our financial leaders offering long considered opinions, the game of predicting financial markets has a way of making us all look like amateurs.

Avoiding Investment Noise

Finally, here’s Warren Buffett in his office and the most striking thing you’ll notice is how basic it is. No technology for charting shares or monitoring financial updates and no TV screen trumpeting the predictions of economists. It’s not what you might imagine from arguably the world’s greatest investor. Given Buffett’s success over the past 50 years his strategy to filter the irrelevant seems to have worked.

Unfortunately, many investors take the opposite approach. They pay attention to the now relentless flow of information and mistake it for actual knowledge. And that ‘knowledge’ comes from the financial media who push the notorious short-term focus of their advertisers – the financial industry.

The financial industry’s intent is to give the impression that trading and reacting to every market movement are normal. At the same time, they purposely ignore the strategies that have been proven to create wealth for investors over the longer term. There’s little point them normalising something that doesn’t make them more money!

Your success isn’t the same as their success. Remember that next time the media tells you “the end is nigh” or some investment will hit big in the future.

With thanks to DFA Australia.

This material is provided for information only. No account has been taken of the objectives, financial situation or needs of any particular person or entity. Accordingly, to the extent that this material may constitute general financial product advice, investors should, before acting on the advice, consider the appropriateness of the advice, having regard to the investor’s objectives, financial situation and needs. This is not an offer or recommendation to buy or sell securities or other financial products, nor a solicitation for deposits or other business, whether directly or indirectly. Looking for the top financial adviser in Australia?