Economic Overview

Q4 2024 was somewhat mixed for Australian investors, but it rounded out what was a positive year across all asset classes. The falling Australian dollar was a tailwind for unhedged investors over the quarter, while the Australian sharemarket was slightly negative. For the year, unhedged global shares, hedged global shares, and Australian shares, all notched double-digit returns. The most notable story across the quarter was Donald Trump’s victory in the US presidential election. This was accompanied by a “red sweep” which saw the Republican Party take control of Congress. As with President Trump’s 2016 election, markets were buoyed by expectations that Trump’s policy positions will increase growth, lower taxes and cut regulation. There were rate cuts in the US, in the Eurozone, and the UK, but they were accompanied by significant bond sell offs in Q4 as yields pushed upward, both locally and globally. Much of this was due to expectations for increased inflation if Donald Trump followed through with many of his economic policies. Other factors were a tax increase in the UK, along with borrowing concerns, ongoing political instability in France, and signals that rate cuts may be slower than previously thought, all combining to push yields up across the globe.

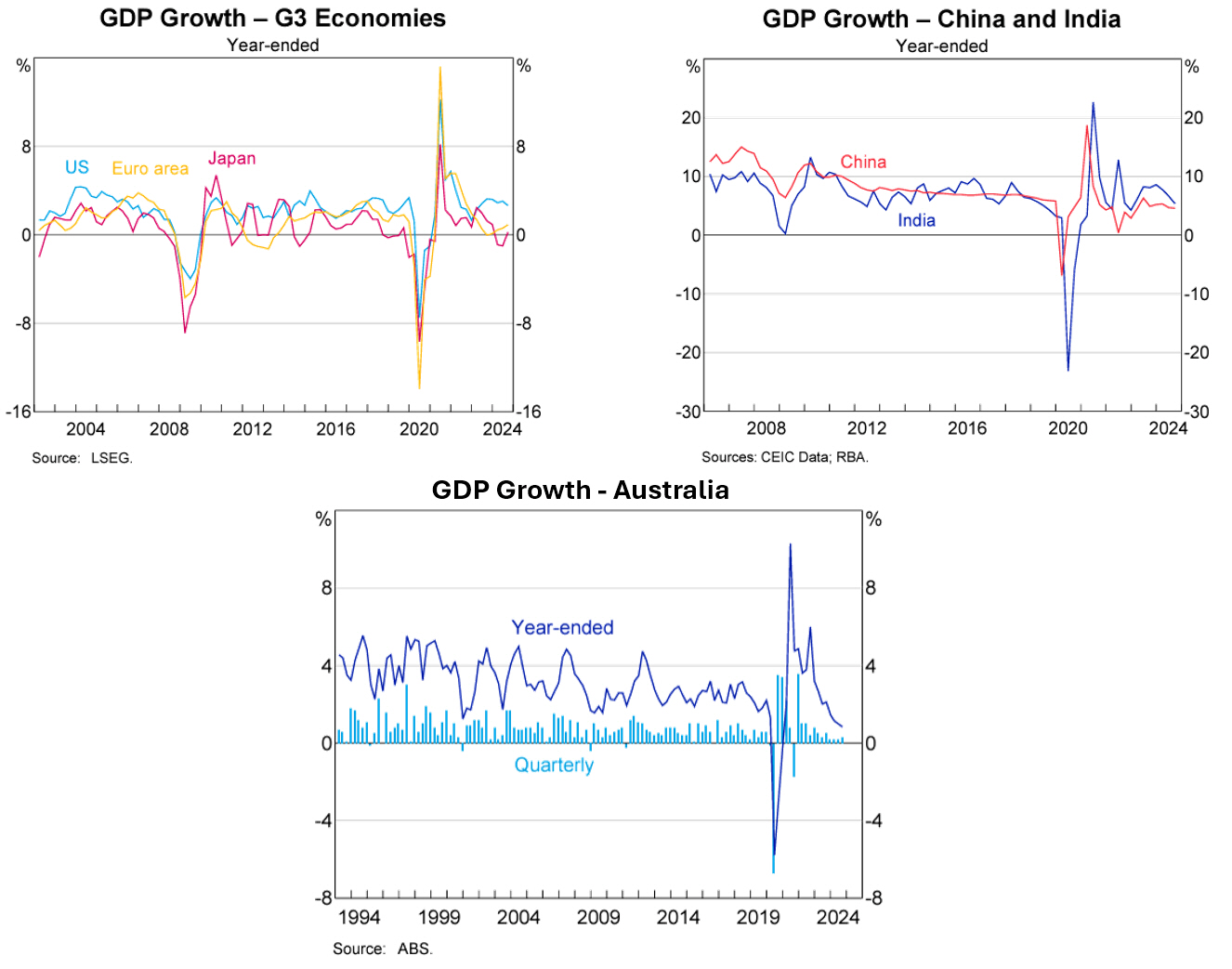

In the US, GDP came in at an annualised rate of 3.1% in Q3 2024, slightly ahead of Q2’s figure of 3.0%, and this marked the strongest GDP figure for 2024. The strongest contributors over Q3 were consumer spending, exports, and federal government spending. There was a downturn in private inventory investment and a decrease in residential fixed investment. The consumer remains resilient as personal spending increased at the fastest pace since Q1 23, with a 5.6% surge in consumption of goods and services. The running estimate of real GDP growth based on available economic data, suggests a Q4 a growth rate of 3.1%.

The labor market remains solid. The unemployment rate was 4.2% in November, and while higher than a year earlier, it remains historically low. With strikes and hurricanes disrupting October, the November jobs report delivered a hiring rebound. Nonfarm payrolls increased by 227k, above expectations, with revisions adding an additional 56k jobs to the prior two months. The private sector contributed 85% of November’s jobs growth, the largest contributors being health care, along with leisure and hospitality. Overall, nearly two million jobs were added in the year to November 24, with wages up 4% year on year.

A couple of years back we discussed the “great resignation”. This was a trend where more than fifty million workers quit their jobs in 2022, as the economy reopened following the pandemic. Employers were desperate to hire, and workers didn’t hesitate to move, attracted by offers of better pay and conditions. Unemployment fell to levels not seen since the late 1960’s, and wages grew at a sharp pace. This has now evolved into what some economists are calling the “great stay”. There is now much less job turnover as the market has cooled. There are also fewer job openings, which has reduced people quitting in search of greener pastures. Business is also more hesitant to lay off workers due to the struggles they had hiring and retaining staff only two years ago. At the moment, this means a strong sense of job security for American workers.

The Federal Reserve delivered two rate cuts during the quarter, trimming the federal funds rate by 0.25% in both November and December. This made it three consecutive meetings with a rate cut. According to forecasts released with the December cut, further cuts are unlikely to come as quickly. Inflation as measured by the Consumer Price Index is now down from 9.1% in June 22 to 2.7% in November, but is still above the preferred goal of 2%. Inflation has also pushed back above the two-year low of 2.4% hit in September. The Fed Reserve is also keenly aware of the potential for tariffs, with Chair Jerome Powell mentioning the inflationary effects of tariffs as a reason some Federal Open Market Committee members may have increased inflation forecasts for 2025.

The major news for Q4 was Donald Trump winning the US Presidential election in November. This is expected to shake up the policy and economic environment. The first 100 days will likely be eventful. A focus will be on extending the Tax Cuts and Jobs Act, but we should expect deregulation and tariffs to feature prominently.

Source: RBA 2024

In the Eurozone, the European Central Bank cut interest rates by 0.25% in both October and December. ECB President Christine Lagarde suggested further cuts were coming in 2025, saying the “direction of travel currently is very clear” as the area continues to struggle with lacklustre growth. Flash PMI data for December showed the private sector ended the year in contraction. Political instability is becoming an ongoing feature in some of the largest Euro countries, with both Germany and France seeing issues throughout 2024. In Germany, the governing coalition collapsed in November after Chancellor Olaf Scholz sacked his finance minister. New elections will be held in February. In France, Prime Minister Michel Barnier’s tenure was short lived. Barnier used executive powers to force through a budget attempting to address a spiralling deficit, which then prompted a no-confidence motion from parties of both the left and right. No new parliamentary elections can be held until July.

In the UK, the honeymoon period for Labour ended very quickly after a landslide election win back in July. An Ipsos poll in December showed 61% of Brits were dissatisfied with PM Keir Starmer, and overall dissatisfaction with the government was at 70%. Over the history of Ipsos, these were the worst ratings seen for a PM and government after 5 months in charge. The economic mood was also abysmal, with 65% of Brits expecting the economic situation to deteriorate over the coming year. Starmer has been hit by a “freebies” scandal after failing to declare gifts, which coincided with widespread disgust over scrapping a winter fuel payment to the elderly, and a higher taxing budget which was perceived to attack farmers. There were also concerns cost increases in the budget are weighing on the jobs market. Hiring data for November showed demand for UK staff had been very weak for a Christmas period. National Statistics data revisions showed the economy had performed worse than expected since the summer, with the ONS revising down Q3 growth to zero from 0.1% previously, while preliminary data from the ONS indicated the economy shrank in October, the second straight monthly contraction.

In Japan, Q3 GDP came in at 0.3% quarter on quarter, down on the downwardly revised 0.5% figure of Q2, annualised growth sat at 1.2% for Q3. Annual inflation sat at 2.7% in November, above market expectations of 2.6%, this was up from 2.3% in October, food prices were mostly to blame for the jump. The Bank of Japan left rates on hold at its December meeting, with BOJ Governor Ueda being less hawkish compared to his speech in July. The move was widely expected given the uncertainty surrounding president-elect Trump’s intentions. Spring wage negotiations, scheduled for March 25, are expected to provide some momentum for wage growth and support an increase in consumption for 2025. Finally, a snap election in late October saw the ruling Liberal Democratic Party and New Komeito coalition lose a majority held since 2012. The result has led to concerns about political stability in Japan, and the wider East-Asia region.

In China, GDP growth for Q3 came in at 0.9%, making it nine consecutive periods of quarterly growth. Year on year Chinese GDP sat at 4.6% for Q3, slightly down on Q2’s 4.7% figure. Core inflation was up 0.3% in November. The People’s Bank of China cut the one-year loan prime rate by 0.25% in October, and it now sits at a record low of 3.1%. Chinese leaders pledged in December to increase the 2025 budget deficit to 4% of GDP in an attempt to spur an economic turnaround and stimulate consumption. They also pledged to shift monetary policy to a moderately loose stance in 2025, moving on from the current “prudent” approach. Most of the China stories during Q4 were external and related to Donald Trump’s vow to impose tariffs of 60% or more on Chinese manufactured goods.

In Emerging Markets, Brazil’s GDP slowed to 0.9% in Q3, down from 1.4% quarter on quarter, but the bigger news was Brazil’s inability to arrest the slide in its currency, which was down more at 20% over the year against the US dollar. While there was an announced program to curb spending, there was also extensive tax cuts promised, which were seen as insufficient commitment to fiscal discipline. South Korea saw significant political instability as both the president, and then the acting president, were impeached during December! Emerging market growth forecasts are 4.2% in 2025. The leader is expected to be India with population continuing to fuel expansion its expansion, with an expected growth rate of 6.8% in the next two years.

Back in Australia, data released in December showed GDP increasing by 0.3% for Q3 2024, with the economy growing by 0.8% for the year ending September. GDP per capita, noted as a proxy for living standards, again fell over the quarter again, down -0.3% and was down -1.5% year on year, marking the seventh consecutive quarter it has gone backwards. Some economic commentators have made the point that immigration driven population growth is masking the reality of Australia’s economic situation. More people are certainly increasing GDP, and hiding a recession, but the public have turned on the Labor government with multiple opinion polls in December showing high disapproval ratings for PM Albanese. The Liberal National Coalition are now ahead on a two-party preferred basis with an election to come in 2025.

Inflation increased 0.2% on a quarterly basis, with CPI coming in at 2.8% for the 12 months ending September 24, down from 3.8% for the year ending June 24. As the Australian Bureau of Statistics noted “the major reason for lower CPI inflation was due to a fall in prices for electricity and automotive fuel”, but this was due to government electricity rebates. Electricity prices fell 17.3% in the September quarter, but excluding the rebates, electricity prices would have risen by 0.7%.

The RBA held the cash rate at 4.35% in it’s November and December meetings. The RBA noted in its December statement that underlying inflation remained too high and “while headline inflation has declined substantially and will remain lower for a time, underlying inflation is more indicative of inflation momentum, and it remains too high.”

House price growth continued to slow over the quarter, and it was a mixed bag for the capital cities, but on an annual basis most markets still increased in value. The combined capitals were up 0.3% and combined regionals were up 1.1% for the quarter. Sydney was down -0.5% for the quarter and up 3.3% annually, according to CoreLogic. Melbourne -1.0%, Darwin -0.7% and Canberra -0.9% also saw falls over the quarter, while Melbourne -2.3%, Hobart -1.0% and Canberra -0.1% were the capitals to see falls over the year. In contrast, Perth was up 21% for the year, Adelaide 14% and Brisbane 12%. Hobart is still down -12.1% since its peak, while Melbourne is down -5.5% since peak. Darwin now sits 7.4% below its peak of May 2014.

Market Overview

Asset Class Returns

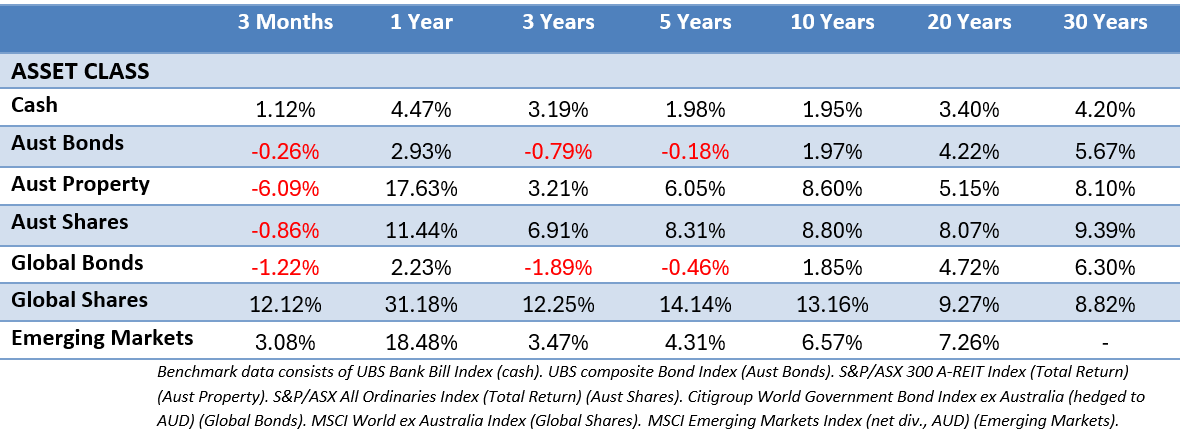

The following outlines the returns across the various asset classes to 31 December 2024.

Global sharemarkets were positive over Q4, but returns for Australian investors were significantly influenced by currency movements. There were mildly positive returns in US large caps, while small caps notched a gain under 1%. In contrast to Q3, the Australian dollar took a tumble and was a tailwind for unhedged returns for Australian investors, but this meant lower returns for hedged investors. The hedged version of MSCI World ex Australia saw a 1.94% return for Q4, while the unhedged index saw a 12.12% return. A 50/50 split between the two, eliminating any currency guesses, delivered a 7% return for the quarter.

The Australian market was down -0.86% for the quarter. Australian listed property continued its zig-zag quarterly movements, down -6.09% after a double-digit gain in Q3, and to put these movements in some context, the A-REIT index in question has 31 companies and the top five companies constitute around 65% of the index, which helps to explain its volatility. Bonds saw falls in Q4 as yields firmed which pushed down prices. The 10-Year US Treasury yield increased throughout Q4, moving from 3.78% to finish at 4.57%. US 2-year Treasury note yields also moved upward sharply in Q4, from 3.64%, to end at 4.25%. It was a similar story in the UK, with the 10-year Gilt yield moving from 4.00% to 4.56%. In Australia the 10-year yield saw similar upward moves, ending at 4.37%, while the 2-Year government bond yield crept up from 3.65% to 3.88% across the quarter.

In the US, the S&P 500 was up 2.41% for the quarter, which rounded out a 25.02% gain for the year. The Magnificent 7 (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla) provided much of the growth across 2024, significantly outperforming the broader S&P 500, with a 48% gain. The S&P 500 excluding the Magnificent 7 saw growth of around 10%, which highlights their current influence. The small cap space resumed tailing large companies during the quarter, with the Russell 2000 only up 0.33% for the quarter, and finished up 11.54% for the year, more in line with the S&P 500 if you excluded the Magnificent 7. The Communications sector was the best performer in 2024, up 40% for the year. Financials delivered a strong return of 30.6% for the year. Consumer discretionary, led by Tesla and Amazon, delivered a strong Q4, up 14%, to end the year up 30%. Utilities increased by 23.4% and technology 36.6%. Industrials and consumer staples saw double-digit gains but tailed the broader market. The big laggards were energy, real estate, health care, and materials with returns below 5%.

In the Eurozone, sharemarkets struggled in Q4 with the MSCI EMU down -1.94% in EU terms, but notched a 9.49% return for the year. Many sectors struggled over Q4 included materials, real estate and consumer staples. One of the few sectors notching a gain were industrials. The headwinds of political unrest, weakening economic data, and dampening business confidence were all an anchor on returns. In France, the CAC 40 was down 3.33% to end marginally down for the year, while despite the political unrest in Germany, the German DAX was up 3.03% in Q4 and finished up 21% for 2024.

In the UK, sharemarkets were flat to negative across Q4, which followed on from a flat to positive Q3. The large cap FTSE 100 was off -0.76%, but up just under 10% for the year. Small and mid sized companies saw losses, with the mid cap FTSE 250 down 2.04%, but up 8.1% for the year, and UK small caps were down 1.39%, but up 7% for the year. Domestically focussed sectors struggled with a rise in long-term bond yields and the concerns about the UK economy. It wasn’t much better for internationally diversified sectors of the UK market, which struggled due to exposure to softening global industrial activity.

In Japan, The Japanese sharemarket saw solid gains during Q4, with the Nikkei 225 up by 5.2%, rounding out a 20% gain for the year. US developments and their ongoing impact on financial markets, particularly the currency market, helped drive the Japanese sharemarket. Weakness in the yen towards the end of 2024 drove a more positive earnings outlook for large-cap exporters. The majority of Japanese companies reported semi-annual earnings results during the quarter, and the results were mixed across various sectors. News of a merger between automakers, Honda and Nissan, along with Toyota announcing a 20% return on equity target, indicated a potential shift in corporate strategies, and that efficiencies will become a significant focus. Share buybacks continued, with many companies announcing additional buybacks which saw favourable market reactions.

Asia (ex-Japan) and Emerging markets struggled in Q4 with multiple headwinds, though thanks to the weakening AUD the MSCI AC Asia ex Japan Index was up 3.22% in Australian dollar terms, while the MSCI Emerging Markets Index was also up 3.08%. Donald Trump’s victory in the US presidential election was a headwind despite US rate cuts, specifically due to investor concerns about the impact of proposed tariffs, particularly on China. China also struggled due to an ongoing lack of detail about policy stimulus announced back in September. Saudi Arabia, Brazil, India and South Africa were negative, while it was the Czech Republic, Kuwait, Taiwan and the UAE leading the way for emerging markets. Taiwan’s performance was again largely driven by positive sentiment around artificial intelligence. Hong Kong also struggled due to Trump and heightened tensions over trade and technology. Singapore was the main winner from the negative sentiment on China and Hong Kong, as overseas investors were attracted by its stability and neutrality.

The Australian market (All Ords Accumulation) was down -0.86% in Q4. While there were more positive sectors than negatives, it was the performance of materials, down -11.75% that dragged the broader index down, as BHP and Rio Tinto both lost ground. Energy and consumer staples also underperformed the index, down -5.22% and -5.33% respectively. Woolworths reported a slip in sales and growth, prompting a cut to its earnings forecast and subsequent share price dip. Financials continued to be strong, the best of the sectors, with a 5.96% return. Commonwealth Bank continued to charge upward, so much so, that its dividend yield is beginning to look anemic. Industrials, communication services, health care, consumer discretionary, IT and utilities all saw gains between 1.5% to 3%. Finally, the ASX Small Ordinaries fell -1.01% over Q4, but finished with an 8.36% return for the year.

This material is provided for information only. No account has been taken of the objectives, financial situation or needs of any particular person or entity. Accordingly, to the extent that this material may constitute general financial product advice, investors should, before acting on the advice, consider the appropriateness of the advice, having regard to the investor’s objectives, financial situation and needs. This is not an offer or recommendation to buy or sell securities or other financial products, nor a solicitation for deposits or other business, whether directly or indirectly.