On the same day rampaging hordes were cutting through the country’s supermarkets, filling their shopping trollies with hundreds of rolls of toilet paper, someone in our office made a call to a well-known superfund.

On this end it was an everyday enquiry on behalf of a client. On that end it was anything but.

“So, you been busy?” We ask. “It’s been flat out. People ringing up to change their allocations,” came the response. Moving from the balanced option and choosing conservative or cash.

Makes you think. And it prompts the question – what do these people know that I don’t?

First, the toilet paper.

Did these people go to the supermarket with the intention of stocking up on toilet paper? Alternatively, did they arrive at the supermarket and see others buying larger than normal volumes of toilet paper and… we’ll let Serena, shopping at an inner-city Sydney Coles explain.

“I thought ‘if everyone’s doing it, I’m doing it too’,” Serena, pushing a trolley packed with paper towels and toilet rolls, said.

“It’s too much, there’s nothing going on… but I have kids at home, so I won’t take the risk if everyone’s buying it all.”

There have been plenty of studies done and papers written on herd like behaviour. We read through a few to write this article. We could summarise those studies and their conclusions, but nothing seems as powerful as Serena’s words.

“I thought ‘if everyone’s doing it, I’m doing it too’.”

Reaction.

And those frantic calls to the superannuation fund?

More reaction.

The simple answer is none of these people know anything. Nothing at all. But they’re looking for something – a sense of control in the face of uncertainty. Why? Because they’re not in the possession of good advice. In the absence of any clarity, people will outsource their decisions to their impulses. Those impulses may be dictated by the wisdom of the crowd or anyone who catches their attention.

Right now, no one is certain of anything. It’s fertile ground for anyone looking to take advantage. Information is ripe for exploitation because few people know who to trust any more. The media is guilty because they turn these events into entertainment. The easiest way to capture and hold attention is sensation.

Six weeks ago, the bushfires seemed unrelenting. They’re now out and a distant memory. The victims are likely now cleaning up their ruined properties and sorting out their lives. The media’s red-hot interest disappeared with the red-hot flames. They now have a virus to capture our attention with.

Despite our criticisms, the media does have a judicious side. Unfortunately, now lost to social media. The person that used to write into the newspaper every day. Their letters were published at the discretion of the editor. The craziest and most inflammatory stuff went in the bin. Today they’re on a social media platform getting directly into the minds of their friends or followers. No filter. Nonsense can move at an unprecedented rate. And there’s little second guessing or consideration.

Why is this an issue?

A study in the Journal of Consumer Research in 2010, called ‘Believe Me I Have No Idea What I’m Talking About’, found as long as an information source is certain of themselves they don’t need to have credibility to be considered persuasive. Similarly, a 2004 study in the Journal of Behavioural Decision Making found that people preferred a financial adviser who appeared extremely confident in their forecasts at expense of other, more moderate and considered advisers.

Anyone promising ‘certainty’, ‘guarantees’ or ‘protection’ usually crawls out from under a rock during these times attempting to exploit fear. And they do it with the utmost confidence. Those without advice are the most vulnerable to the nonsense flying around. The nonsense may come from an amateur on their soapbox or a ‘professional’ looking to make a dollar.

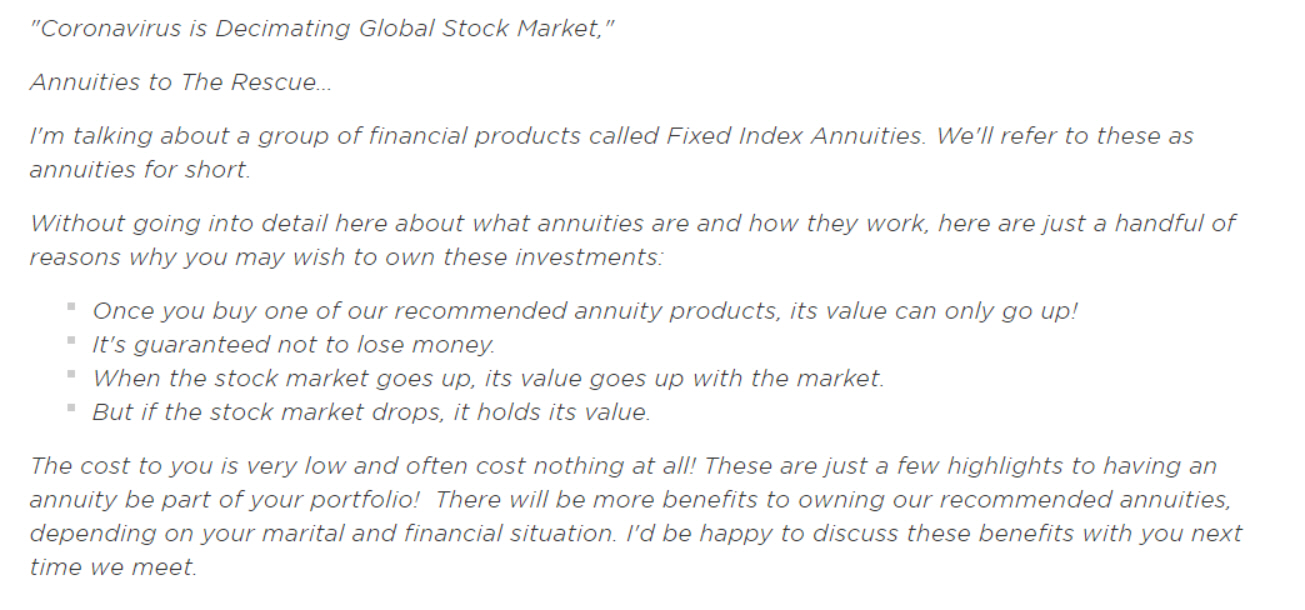

The following is part of an email that went to schoolteachers in the US. It’s using the coronavirus to manipulate them into making changes in their retirement account.

Short explanation: A tax deferred product put in a tax-sheltered account. No need. Wholly unsuited for a long-term saver who needs growth, not income. Fees that can range from 3-4% and another 6-7% to exit the product early. All to avoid market volatility. This ‘rescue’ email came from an annuity salesperson on a 6% commission. All investors should be wary of those promising safe havens as long as the Coronavirus lasts.

There’s a reason we recommend doing nothing.

A portfolio exists to support a plan and a plan exists to support goals.

The risk taken in a portfolio is aligned with those goals over a certain time frame. Returns are not guaranteed, but something we reasonably expect over that time frame. Returns never occur in a linear manner, nor do we expect them to. There are many paths to achieve (for example) a 7% per annum return over a ten-year period.

If that’s what you need to achieve your goals one thing is assured – it won’t be happening in cash.

You might say this is the least worst system above all others. The painful part is the volatility, but the fact a portfolio moves around is evidence it’s working.

As for the nonsense, it will be here for a while.

That much is certain.

This represents general information only. Before making any financial or investment decisions, we recommend you consult a financial planner to take into account your personal investment objectives, financial situation and individual needs.