It’s been a few weeks of recollection. A decade on since the anniversary of Lehman Brothers collapsing and one of the touchstone moments of the ordeal is being not so fondly remembered.

No one really knew if it was the beginning of the end, an ongoing crisis or not far from a recovery. History shows the market bottom took another six months and if you could stand the uncertainty you got the recovery.

Today the media seems to be asking all the wrong questions and specifically canvassing for when the next crisis may hit. Usually, it’s just the kooks who are out, year after year, suggesting the next crash is only moments away. When it’s a significant anniversary since the last moment of doom, the rolled gold big timers get off their seat to weigh on how close we came and when the next crisis will appear.

It’s not particularly helpful because their predictive abilities are no better just because they reserve their judgements for special occasions. Unfortunately, investors may well give weight to these calls. The events of a decade ago weren’t particularly pleasant and no one wants to relive them, but if you look across history, something of that enormity doesn’t happen on a regular basis.

If you were an investor during 2008, it’s an event that would have unquestionably had some emotional impact upon you. Financial advisers across the world have stories of the clients who couldn’t stand the relentless barrage of disastrous news coupled with the market and portfolio declines. Eventually they bailed to cash.

That includes us. We lost a client and had another two decide cash was the best place to be.

Given the unprecedented nature of the event, maybe you couldn’t blame them, but selling in the midst of crisis never works out well. Selling in the midst of a once in a century crisis? That would work out even worse. It was too late to avoid any loss, so a sale in the midst of terror only crystalised the loss and ensured there would be no recovery.

Come October 2008 the seeds of the recovery were planted. The $700 billion Emergency Economic Stabilization Act of 2008 passed US Congress, and the recovery was sparked. Not long after the Dow gained 936 points, or 11%, for its greatest one-day advance. Two weeks later come the second-largest gain in history as the Dow put on 889 points, or another 11%.

Volatility was far from over. World markets continued to spill downwards. Respite truly came in March 2009. Many who bailed did so close to the bottom. That has to hurt, but the whole experience was painful. So much so, the scars may even be showing up in those who hadn’t started investing back then.

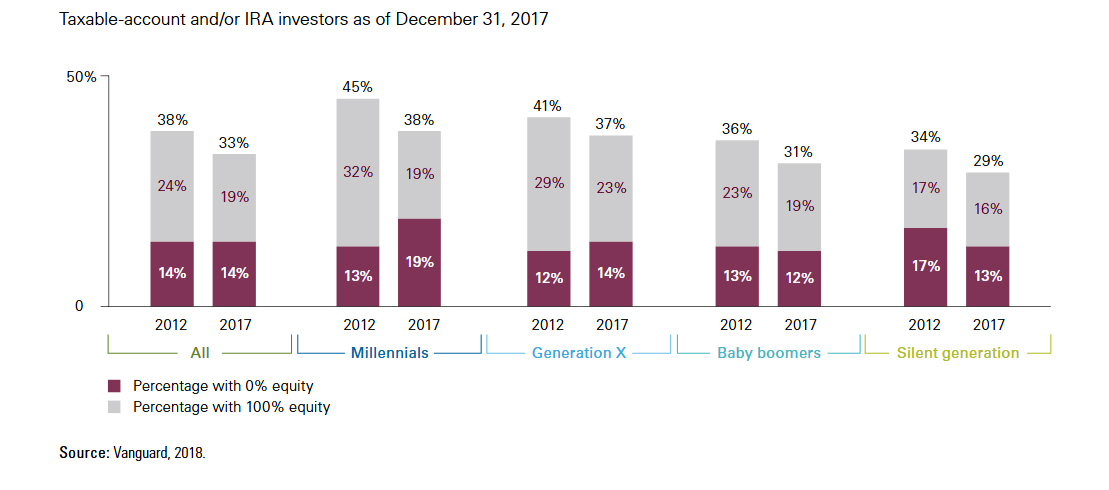

Back in June Vanguard published a paper entitled ‘Risk-taking across generations’. One of the more interesting points was, out of any demographic investing with Vanguard in 2017, the millennials were the most likely to have a zero-equity portfolio, with 19% of all millennial accounts having no equity exposure.

This isn’t just a rogue finding. Back in 2014, UBS found the average investor between the ages of 21-36 had 52% of their savings in cash. As UBS noted:

Investors of all generations are most likely to have a moderate risk tolerance. But Millennials and WWII generation investors are more likely to describe themselves as truly conservative. This is remarkable given the impact the Great Depression had on the WWII generation and speaks to the potential permanent scarring that 2008 had on the Millennial investor.

This is consistent with a paper by Ulrike Malmendier and Stefan Nagel entitled “Depression Babies: Do Macroeconomic Experiences Affect Risk-Taking?” completed for the National Bureau of Economic Research. The pair suggested that people who’ve experienced high stock market returns throughout their lives are more likely to invest in the stock market. While they suggest recent events are the most powerful, early experiences still have an influence over investment behaviour. As they noted:

Economic events experienced over the course of one’s life have a more significant impact on individuals’ beliefs or preferences than historical facts learned from summary information in books and other sources.

It doesn’t have to be this way though. From our own perspective we see a great divergence between the knowledge base and emotional control of clients who work with us vs the general community. Someone who walks in the door for the first time is rightly skeptical and sometimes confused. We use a relatively simple evidence-based process, it doesn’t guarantee anything, but we believe it’s the most reliable way to build wealth long term.

It doesn’t immediately translate. The majority of what people know of investing are media reports. Where the market has $60 billion ‘wiped’ in a day. Where people are ripped off left, right and centre. Those are the ongoing disaster stories. The balance? The success stories the media focus on are usually get rich quick schemes or strategies built on sand.

For lack of a better term, there’s some reprogramming and education that needs to happen. It’s having emotional resilience and a knowledge base that aligns with an evidence-based investment philosophy that gives someone a better chance of success.

Those who trusted their adviser’s word got through the worst crisis they’ll ever see. Those who didn’t are unfortunately still stuck back in 2008 waiting for the next big one.

This represents general information only. Before making any financial or investment decisions, we recommend you consult a financial planner to take into account your personal investment objectives, financial situation and individual needs.