As a year ends and new one begins, there’s usually a period of reflection. If things went well, we can pat ourselves (and others, if we’re generous) on the back for our achievements. If things went poorly, it can be a simple admission that we can’t always win before quickly moving on. Or it might be changes and recriminations that result from a poor year.

Good years when investing are expected, it’s why we invest. Poor years when investing aren’t welcome. When investing, returns are the primary concern of investors. Returns are judged by time periods. A month. A quarter. Half a year. A year. As every new year rolls around, financial advisers will inevitably see some extra inquiries as people look to get their finances sorted and resolve to get their money and investments sorted out.

There are always a few extra inquiries through January, but after a bad year there are more tire kickers than usual.

It might be the investor who got their portfolio ideas from an internet forum. It might be an investor who has an adviser. Both portfolios might be absolutely fine, but it’s the bad year that throws each into question. A simple question is often behind looking around after poor year “can these guys do better than my current portfolio or adviser?”

Of course, we’ll say we’re the best. Our colleagues who share the same ideas and philosophies are also the best. But there are no guarantees of doing better on performance by changing to something or someone new. Performance can’t be guaranteed. It can’t be cajoled or prompted. It doesn’t run on schedules or expectations. Better off to ensure your portfolio is aligned with your goals, it’s tax efficient and the fees are kept to a minimum. That’s part of good advice.

If an investor has expectations and measures them by what occurs between January 1 and December 31 of any particular year, on average they will be disappointed every one out of four years if looking at equities. Investors can have a rigorously constructed portfolio, backed by all the evidence and sooner or later it will still have a year that disappoints. Investors can control what they can, but they can’t control everything. Performance falls into that basket.

Any investor who was a little irritated by the end of December 2022 and looking to change things, may have found themselves reconsidering by the end of January 2023. The S&P 500 was up 6.28% and the ASX All Ords was up 6.44%. It shouldn’t have made a difference to anyone’s investment strategy, but a reprieve is a reprieve. Does it mean anything?

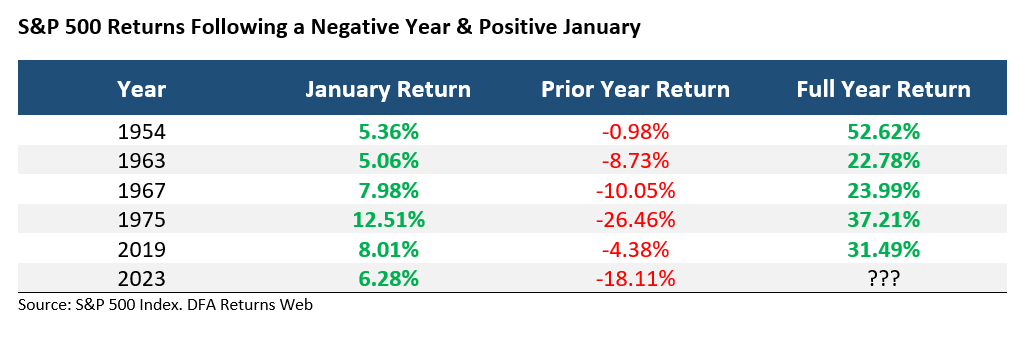

In the US, there is something known as the January Barometer. Essentially the S&P 500 has a tendency to have a positive year after it has a positive January. It inspired the term “as January goes, so goes the rest of the year”. Starting back in 1927 gives us 96 years to look at. Almost 73% of years are positive. When January is positive, 84% of the time the full year has also been positive.

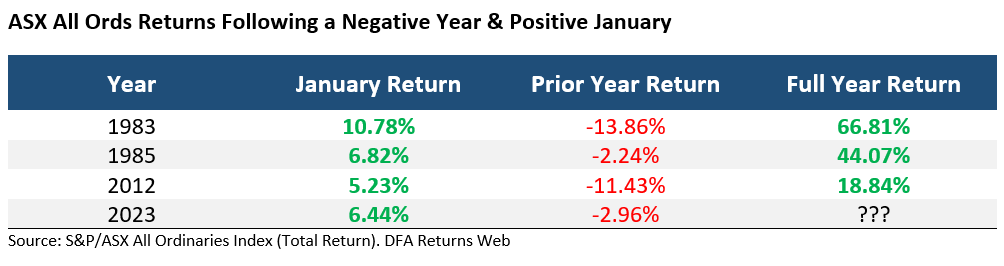

How does this measure up in Australia? Starting in 1980 offers data that includes months, so we can see January returns. Starting in 1980 which gives us 43 years. Since 1980 just over 73% of years on the ASX All Ords are positive. When January is positive, 80% of the time the full year has also been positive.

Anything else we can glean?

Well yes, while looking through this data we noticed something else. Specifically, about very positive starts to the year that followed on from a prior negative year. On the ASX, if the prior year was negative, and January of the following year posted a return of 5% or better, that year would go on to post exceptional returns.

It was a similar story on the S&P 500. If the prior year was negative, and January posted a better than 5% return, then that year also posted exceptional returns. Double digits in every instance.

It’s not to say any of this is guaranteed, but if it doesn’t happen in 2023 it will be the first time on either index that a negative year, followed by a 5%+ January, didn’t go on to post a double digit return for the full year.

There are plenty potholes ahead we can see, plus there are always surprises that we won’t see. Whatever happened last year is long gone, those considering their options after December shouldn’t, nor should they need to reconsider after a good January. Investing needs a longer horizon than that.

US investment manager Cliff Asness recently summed this up neatly, “anything you’re not going to stick with isn’t a good idea, even if it’s a good idea.”

Before making any financial or investment decisions, we recommend you consult a financial planner to take into account your personal investment objectives, financial situation and individual needs. Looking for financial advice in Canberra? Mancell Financial now have an office in Bungendore just outside Canberra, servicing the region.